Easy to use

It is based on very solid mathematical formula, yet very easy to use.

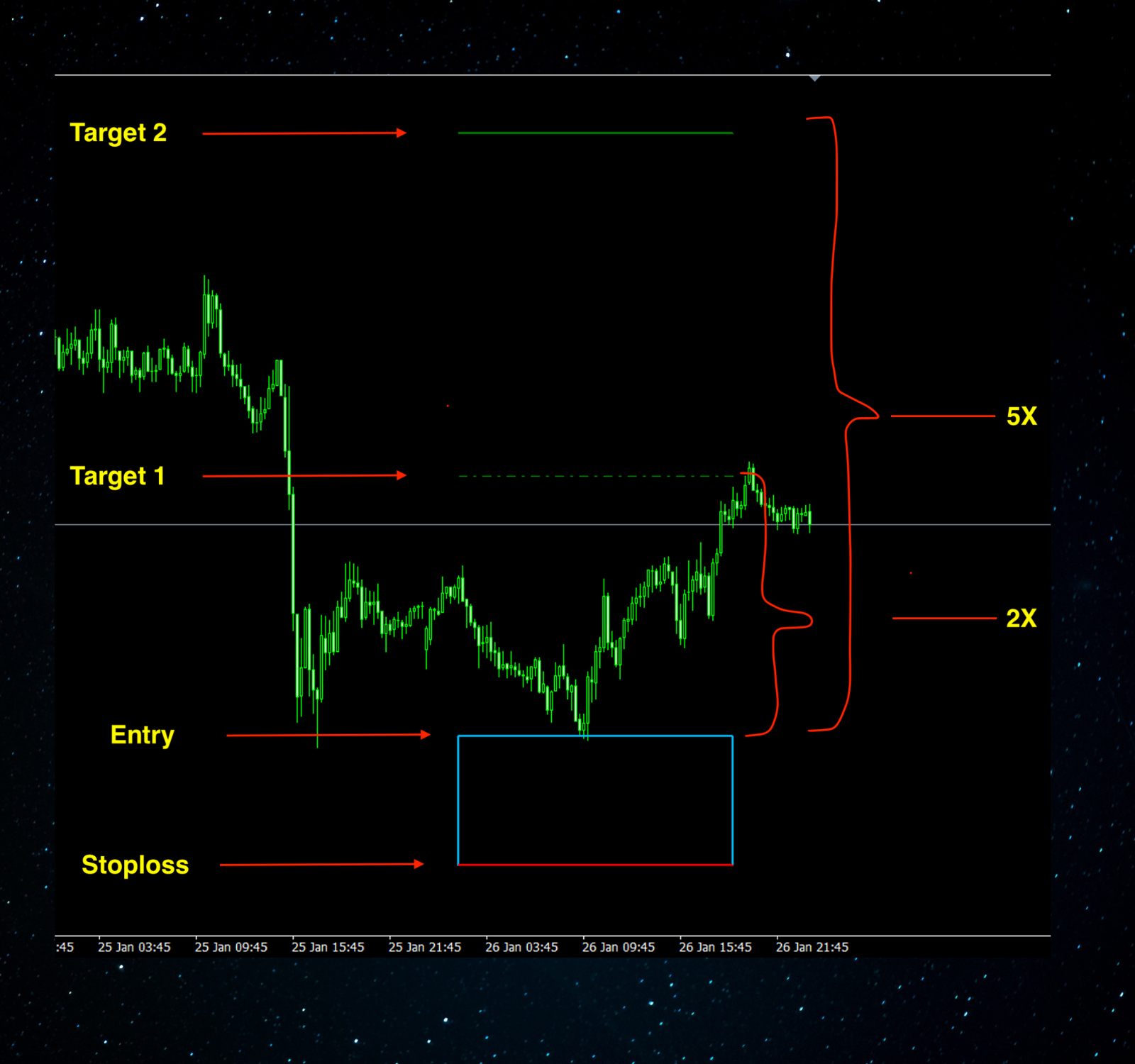

Non Repainting

Once the trading zone and the targets have been determined they are valid for the whole day.

Tested Winner

The T5X indicator has proved itself in live trading. It can make trading easier and more profitable.

John Miller

Investment Banker“I've been using Target 5X indicator for the past year, and it's been a game-changer for my trading strategy. The simplicity of the box, stop-loss, and target approach is refreshing, and it allows me to focus on the bigger picture without getting bogged down in complex indicators. I appreciate the clear risk-reward profile, with the first target offering a chance to secure quick profits and the second target aiming for significant gains. Overall, [Indicator Name] has helped me become a more disciplined and confident trader.”

Sarah Jones

Financial Analyst“As a busy professional, I don't have time to spend hours analyzing charts. T5X is a perfect fit for my needs - it's easy to understand and implement, but still provides valuable insights. The visual representation of the box and targets is particularly helpful, allowing me to quickly identify potential trade opportunities. I've found that [Indicator Name] has helped me improve my trading accuracy and profitability, while also saving me valuable time.”

David Lee

Day Trader“I've tried many different indicators over the years, but Target 5X stands out for its simplicity and effectiveness. The clear entry and exit signals provided by the box and stop-loss levels have helped me to avoid emotional trading decisions and stick to my trading plan. The two profit targets offer flexibility, allowing me to take profits when they become available or hold on for potentially larger gains. I highly recommend [Indicator Name] to any trader who wants a straightforward and reliable tool to improve their trading results.”

John Miller

Investment Banker“I've been using Target 5X indicator for the past year, and it's been a game-changer for my trading strategy. The simplicity of the box, stop-loss, and target approach is refreshing, and it allows me to focus on the bigger picture without getting bogged down in complex indicators. I appreciate the clear risk-reward profile, with the first target offering a chance to secure quick profits and the second target aiming for significant gains. Overall, [Indicator Name] has helped me become a more disciplined and confident trader.”

Sarah Jones

Financial Analyst“As a busy professional, I don't have time to spend hours analyzing charts. T5X is a perfect fit for my needs - it's easy to understand and implement, but still provides valuable insights. The visual representation of the box and targets is particularly helpful, allowing me to quickly identify potential trade opportunities. I've found that [Indicator Name] has helped me improve my trading accuracy and profitability, while also saving me valuable time.”

David Lee

Day Trader“I've tried many different indicators over the years, but Target 5X stands out for its simplicity and effectiveness. The clear entry and exit signals provided by the box and stop-loss levels have helped me to avoid emotional trading decisions and stick to my trading plan. The two profit targets offer flexibility, allowing me to take profits when they become available or hold on for potentially larger gains. I highly recommend [Indicator Name] to any trader who wants a straightforward and reliable tool to improve their trading results.”

John Miller

Investment Banker“I've been using Target 5X indicator for the past year, and it's been a game-changer for my trading strategy. The simplicity of the box, stop-loss, and target approach is refreshing, and it allows me to focus on the bigger picture without getting bogged down in complex indicators. I appreciate the clear risk-reward profile, with the first target offering a chance to secure quick profits and the second target aiming for significant gains. Overall, [Indicator Name] has helped me become a more disciplined and confident trader.”

Sarah Jones

Financial Analyst“As a busy professional, I don't have time to spend hours analyzing charts. T5X is a perfect fit for my needs - it's easy to understand and implement, but still provides valuable insights. The visual representation of the box and targets is particularly helpful, allowing me to quickly identify potential trade opportunities. I've found that [Indicator Name] has helped me improve my trading accuracy and profitability, while also saving me valuable time.”

David Lee

Day Trader“I've tried many different indicators over the years, but Target 5X stands out for its simplicity and effectiveness. The clear entry and exit signals provided by the box and stop-loss levels have helped me to avoid emotional trading decisions and stick to my trading plan. The two profit targets offer flexibility, allowing me to take profits when they become available or hold on for potentially larger gains. I highly recommend [Indicator Name] to any trader who wants a straightforward and reliable tool to improve their trading results.”